Audit Risk Model Explained: Formula, 3 Lines & Detection Risk

Robin Joseph

Senior Security Consultant

Ever wondered how auditors decide where to focus their attention? Or why some organizations face far more scrutiny than others during audits?

That decision-making isn’t random. It’s guided by a structured framework that shapes audit planning from day one.

The audit risk model acts like a GPS for auditors. It helps them decide where to look closer, what evidence to collect, and how rigorous their testing needs to be. Its real value shows up early—during planning—when audit strategies are formed and resources are allocated. Once fieldwork begins, the model has already done its job.

What makes this approach so effective is its focus. Instead of treating every area the same, auditors use risk signals to prioritize effort. High-risk areas get more attention. Lower-risk areas get less.

This risk-driven mindset isn’t just theoretical. It influences how audits are scoped, how controls are evaluated, and how confident auditors can be in their final conclusions.

Understanding the Audit Risk Model

The audit risk model is a planning framework that helps auditors decide where things are most likely to go wrong. Instead of applying the same level of scrutiny everywhere, it gives auditors a structured way to assess risk and allocate effort where it matters most.

The model works by breaking overall audit risk into three connected components: inherent risk, control risk, and detection risk. Each component answers a different question—how risky an area is by nature, how well the organization’s controls manage that risk, and how likely audit procedures are to catch remaining issues.

What makes the audit risk model powerful is how these pieces interact. Higher inherent or control risk means auditors must lower detection risk through deeper testing and stronger evidence. Lower risks allow for more streamlined procedures. This balance is what turns audit planning from guesswork into a disciplined, risk-based process.

Breaking Down the Audit Risk Model Formula

Auditors don’t rely on guesswork—they use the audit risk model to plan effectively. This framework turns risk judgment into actionable numbers, helping auditors decide where to focus, how much evidence to gather, and which procedures to apply. It’s especially useful during audit planning, guiding resource allocation, testing depth, and evidence requirements.

Audit Risk Model Formula

The core formula is:

Audit Risk (AR) = Inherent Risk (IR) × Control Risk (CR) × Detection Risk (DR)

Each component has a distinct purpose:

- Inherent Risk (IR): The natural likelihood of errors or fraud before any controls exist

- Control Risk (CR): The chance that internal controls fail to prevent or detect misstatements

- Detection Risk (DR): The likelihood that auditors’ procedures miss a material misstatement

Detection risk is the variable auditors can directly manage. Higher inherent or control risks mean auditors must reduce detection risk through stronger testing and more evidence.

Audit Risk Model Formula vs Risk of Material Misstatement Formula

Another version is:

Audit Risk (AR) = Risk of Material Misstatement (RMM) × Detection Risk (DR)

Where RMM = IR × CR

- RMM reflects the client’s exposure to risk before audit work begins

- AR combines client-side risk with the auditor’s ability to detect it

Think of it this way: RMM is the client’s “baggage,” AR measures whether the auditor will notice it.

How the Audit Risk Model Formula Guides Audit Planning

The model drives key planning decisions:

- Resource allocation: Focus auditors on high-risk areas, not low-risk zones

- Procedure selection: Higher inherent or control risks call for more extensive testing

- Evidence gathering: Different risk levels determine how much and what type of evidence is needed

Example: A firm with 5% acceptable audit risk, 90% inherent risk, and 40% control risk calculates 14% detection risk. Audit procedures must keep detection risk below this threshold to achieve the target.

The audit risk model is a roadmap. It tells auditors where to dig, how hard to dig, and how much evidence is enough. No guesswork—just structured, risk-based auditing.

Inherent, Control, and Detection Risk Explained

Each piece of the audit risk puzzle behaves differently. Understanding them helps auditors focus effort where it matters most.

Inherent Risk: Complexity and Susceptibility to Misstatement

Inherent risk is the natural likelihood of errors or fraud in financial statements, before any controls are applied. Some businesses are just riskier than others. Key drivers include:

-

Transaction complexity: Complex revenue recognition or derivative accounting carries higher risk than simple cash transactions

-

Industry characteristics: Banking, finance, and regulated industries face elevated risk due to volume and regulatory changes

-

Accounting estimates: Areas needing judgment like loan loss provisions or warranty reserves

-

Management integrity: Bias, pressure, or intentional misstatements

Auditing standards highlight five factors: complexity, subjectivity, change, uncertainty, and susceptibility to management bias. If a business involves guesswork or frequent change, inherent risk is high.

Control Risk: Weaknesses in Internal Controls

Control risk is the chance that a company’s internal controls fail to prevent or detect misstatements. Common causes include:

- Poor segregation of duties

- Weak supervision or monitoring

- Flawed control system design

- Human error in financial reporting

Entity-level control weaknesses are particularly dangerous—they can render process-level controls ineffective. A broken control environment amplifies risk across the organization.

Detection Risk: Interaction and Impact

Detection risk is the likelihood that audit procedures fail to catch a material misstatement, and it’s the only risk auditors can directly control. When inherent and control risks are high, auditors reduce detection risk by:

- Using more effective audit procedures

- Expanding sample sizes

- Performing detailed substantive testing

Lower detection risk requires more evidence. This relationship guides testing strategy, resource allocation, and overall audit effort. High-risk areas demand deeper scrutiny—auditors can’t rely on luck.

Bottom line: Inherent, control, and detection risks shape every audit decision. Understanding them ensures auditors focus effort effectively and keep overall audit risk within acceptable levels.

Using the Audit Risk Equation in Planning

Theory’s nice, but how do auditors actually use the audit risk equation? Once inherent and control risks are assessed, auditors can calculate the maximum detection risk allowed to keep overall audit risk within acceptable limits.

How to Adjust Detection Risk Based on Control Risk

Detection risk moves opposite to material misstatement risk (IR × CR). This relationship drives audit planning:

- High control risk → detection risk must be low: more extensive substantive testing

- Low risk areas → detection risk can be higher: auditors can ease up on testing

- Lower detection risk → more evidence needed

Auditors adjust detection risk by changing:

- Nature of procedures (analytical vs detailed testing)

- Timing of tests

- Extent of testing (sample size, depth of procedures)

Example: Acceptable audit risk 4%, inherent risk 80%, control risk 100% → detection risk = 5%. That gives 95% assurance that financial statements are accurate.

Using the Audit Formula in Compliance Audits

The same principles apply beyond financial audits. For instance, a healthcare company handling sensitive patient data:

- Inherent risk: 70%

- Control risk: 50%

- Detection risk: 25%

Final audit risk = 0.7 × 0.5 × 0.25 = 8.75%

This lets compliance teams:

- Focus on the riskiest areas first

- Prioritize controls to implement next

- Reduce overall audit risk methodically

Even when control weaknesses are high, quantifying them shapes testing strategy and ensures critical procedures aren’t skipped.

The audit risk formula is a roadmap for both financial and compliance audits, helping teams plan testing, allocate resources, and strengthen internal controls. No guessing—just disciplined, calculated action.

Integrating the 3 Lines of Defense in Audit Risk Management

Math alone won’t protect you. The audit risk formula is useful, but effective risk management requires strong governance, and that’s where the Three Lines Model comes in—a framework that clarifies who owns and manages risk.

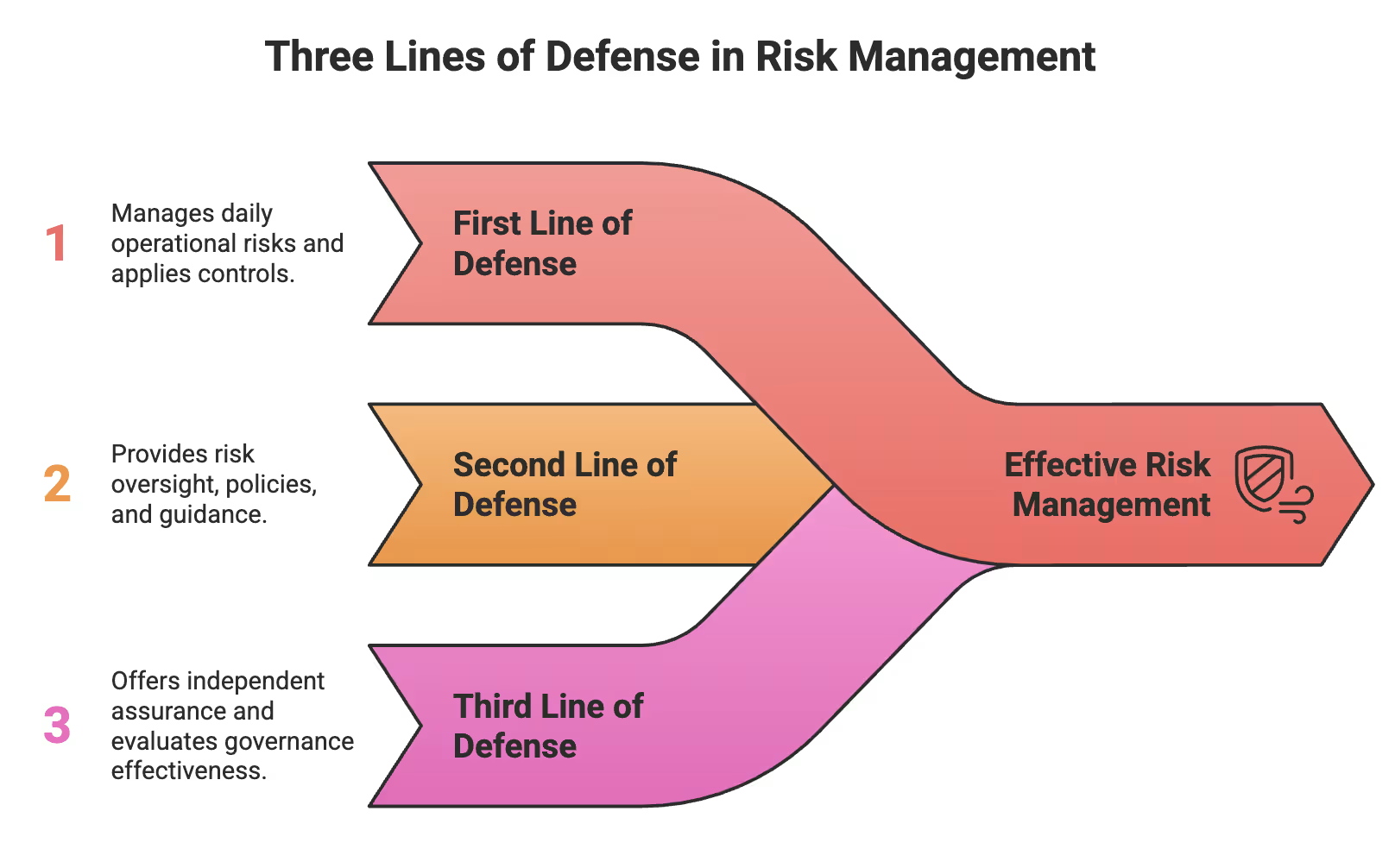

3 Lines of Defense Model Overview

The Three Lines Model (formerly Three Lines of Defense) defines roles and responsibilities for risk management across an organization:

- First line: Employees and managers handling day-to-day operations

- Second line: Risk and compliance teams providing oversight and guidance

- Third line: Independent audit offering objective assurance

Without clarity, overlaps and gaps appear. The model works across industries but must be tailored to your organization.

First Line: Operational Risk Ownership

The first line owns and manages risks in daily operations. They are the frontline defenders, applying controls and monitoring processes as work happens.

They:

- Use controls actively, not just follow procedures

- Continuously observe operations

- Report risks or anomalies to management

Even simple tasks, like inventory counts or transaction checks, directly reduce errors and misstatements. This line forms the foundation of risk management.

Second Line: Risk Management and Compliance Oversight

The second line provides specialized risk support, policies, and oversight. They are close enough to operations to see problems but independent enough to challenge management.

They:

- Build risk frameworks and policies

- Monitor high-risk areas and emerging threats

- Evaluate activities against organizational risk appetite

When issues arise, they direct control adjustments and guide the first line.

Third Line: Independent Audit and Assurance

The third line offers objective assurance, independent of management. Internal audit reports directly to the board, ensuring credibility.

Their role:

- Assess governance and risk management effectiveness

- Identify gaps and recommend improvements

- Strengthen accountability across the organization

By providing independent assurance, the third line ensures that both operational and oversight efforts are effective, closing gaps and reinforcing accountability across the organization.

How the 3 Lines of Defense Assurance Model Reduces Audit Risk

This framework lowers audit risk by clarifying roles:

- Control risk drops because responsibilities are clear and owned

- Detection risk decreases through independent assessments and direct reporting

Implementing the model effectively fosters collaboration, eliminates duplication, and builds a robust risk framework that protects the organization beyond compliance checklists.

Real-World Applications of the Audit Risk Model

Theory’s great, but how does this work when the rubber meets the road? Let’s look at businesses using these concepts to make audit decisions that actually matter.

Audit Risk Model Calculation Example with Percentages

Imagine a healthcare company handling sensitive patient data in a complex cloud setup.

Numbers tell the story:

- Inherent risk (IR): 70%, high due to PHI exposure

- Control risk (CR): 60%, medium-high with MFA but missing role-based access

- Detection risk (DR): 24%, based on system limitations

Plug it in: AR = IR × CR × DR = 0.70 × 0.60 × 0.24 = 0.1008 (10.08%).

Auditors now know where to focus—no guesswork, no flying blind. This calculation informs which areas need more testing and which controls need attention.

Aligning Audit Risk Model with 3 Lines of Defense Responsibilities

Smart organizations sync their audit risk approach across all three lines:

- First line (operational): Hourly-to-daily work, implementing controls, monitoring continuously

- Second line (tactical): Weekly-to-monthly tasks, setting risk goals, identifying emerging issues

- Third line (strategic): Quarterly-to-yearly independent analysis against standards

This timing-based alignment reduces overlaps and gaps.

The payoff? Teams stop duplicating work, continuous monitoring catches anomalies early, and overall audit assurance increases. Confidence levels rise because audit risk is quantified, and organizations can adapt the model as they grow.

Balancing Audit Risk and Audit Assurance

Audit balance isn’t neat. It’s messy—and that’s exactly what separates the pros from the wannabes. You can’t just plug numbers into a formula and call it a day. Real audit effectiveness comes from understanding how risk and assurance interact.

What is Acceptable Audit Risk?

Acceptable audit risk is your comfort zone with uncertainty—the amount of risk auditors are willing to accept when giving a clean opinion on financial statements that might actually have issues.

- High-stakes audits: Low risk tolerated

- Professional standards: Keep risk low enough to feel confident in your opinion

- Practical reality: Constantly juggling the audit risk model to find the sweet spot

Understanding acceptable audit risk lays the foundation for calculating audit assurance and planning procedures effectively.

Audit Assurance and Its Relationship to Audit Risk

Audit assurance tells you how confident your audit really is. The math is simple:

Audit assurance = 100% - Acceptable audit risk

For example, if acceptable audit risk is 5%, you’re delivering 95% assurance. Higher assurance demands lower acceptable risk. This relationship helps auditors communicate confidence to stakeholders and informs decisions about testing strategies.

Balancing Audit Risk and Materiality Thresholds

Here’s where judgment comes in. Multiple factors interact:

- Higher risk → more evidence required

- Lower materiality → more precise testing

- Risk and materiality move inversely: Less risk may mean testing fewer items

The sweet spot? High-risk, low-materiality areas get full attention. Low-risk, high-materiality areas can be audited more lightly.

Balancing risk, assurance, and materiality isn’t about following rules blindly. It’s about developing the intuition to know when to push harder, when to pull back, and how to use the audit risk model to make smarter, defensible audit decisions.

Conclusion: Strengthening Audit Quality Through Risk Awareness

The Audit Risk Model is not a theoretical framework meant to sit on a shelf. It is a practical tool that helps auditors identify, assess, and manage risk with structure and intent. By converting judgment-based concerns into a disciplined approach, the model allows auditors to focus effort where it matters most and use resources efficiently.

Its three components—inherent risk, control risk, and detection risk—work together to shape audit strategy. Detection risk is the one lever auditors can directly control. When inherent or control risk is high, detection risk must be reduced through deeper testing and stronger evidence.

The model becomes more powerful when combined with the Three Lines Model. Clear ownership across operations, risk management, and independent assurance reduces gaps and avoids duplication.

Balancing acceptable audit risk with audit assurance requires both analysis and judgment. The equation is simple, but the impact is significant. Used correctly, the Audit Risk Model leads to stronger audits, better governance, and greater stakeholder confidence.