PCI DSS Compliance for FinTech Startups

Robin Joseph

Senior Security Consultant

Ever wondered why PCI DSS compliance feels like navigating a maze blindfolded? You’re not alone. PCI DSS isn’t just another acronym floating around in the payments world—it’s the rulebook that keeps cardholder data safe from the bad guys.

It was born in 2006 from the collective muscle of Visa, Mastercard, American Express, Discover, and JCB. What started as a shared standard quickly became the backbone of modern payment security.

And if you’re running a fintech startup? Understanding PCI DSS isn’t optional. It’s survival. According to the National Cyber Security Alliance, 60% of small businesses hit by cyberattacks shut down within six months. And in 2023 alone, over 63% of fintech breaches involved stolen payment card data—usually because basic security controls were missing.

The part most founders underestimate? PCI DSS applies to anyone touching card data—processors, digital wallets, BNPL platforms, mobile payment apps. Even if you outsource payments, you’re still responsible for keeping your environment compliant.

But here’s the upside: build PCI controls early, and you’re not just checking a box. You’re laying the groundwork for secure, scalable growth—without the constant fear of the next breach.

Key Takeaways

- PCI DSS compliance is mandatory for any fintech that accepts, processes, stores, or transmits card data — outsourcing payments reduces scope but not accountability.

- Choose the right Self-Assessment Questionnaire (SAQ A, A-EP, or D) based on how your application interacts with payment data — most SaaS fintechs need SAQ A-EP.

- Automation cuts compliance effort by up to 80% — tools like Secureframe, Scrut, and Hyperproof handle evidence collection, monitoring, and reporting.

- Tokenization and network segmentation are the fastest ways to shrink your PCI scope and reduce audit burden.

- Start early — embedding PCI controls from day one turns compliance into a growth advantage, not a bottleneck.

Is PCI DSS Mandatory for Startups?

If your startup touches card data, PCI DSS isn’t optional. It’s the rulebook you can’t ignore. Not a law—but banks and card networks treat it like one.

The moment you accept, process, store, or transmit cards, PCI requirements kick in. Size, funding stage, or age of your startup doesn’t matter. Skip it, and the fallout is real: fines, audits, higher processing fees, or frozen accounts.

Outsourcing payments helps, but it doesn’t hand off responsibility. Stripe, Razorpay, or another gateway may reduce scope—but accountability stays with you. Every card, every access point, every server storing data—that’s on your startup. Shared-responsibility gaps are where most early-stage fintechs stumble.

In our work with early-stage fintechs at UprootSecurity, we’ve seen this firsthand: startups that embed PCI requirements early don’t just survive. They move faster, earn trust sooner, and scale without painful security headaches. Compliance becomes a growth engine, not a roadblock.

Understanding PCI DSS Compliance for FinTech Startups

PCI DSS sounds intimidating, but at its core, it’s a practical framework for protecting payment card data anywhere it lives, moves, or gets processed. It’s not government law, but banks and card networks treat it as non-negotiable. If you accept, store, process, or transmit card information in any form, you’re automatically in scope.

For fintech startups, PCI DSS matters for one reason: your business runs on trust. Investors expect it. Partners demand it. Customers assume it. Skip compliance and you’re staring at penalties from $5,000 to $100,000 per month, plus breach costs that can easily climb into the millions.

The standard outlines 12 requirements across six pillars—network security, data protection, vulnerability management, access control, monitoring, and policies. Yes, it can feel heavy. But startups that integrate these controls from the start turn PCI DSS into an advantage, not a roadblock. It becomes the guardrail protecting your product, your customers, and your credibility as you scale.

Determining Your PCI Compliance Scope and Level

Look, you can’t jump into PCI compliance blindly. Three things determine what you’re actually on the hook for: how your business operates, how many transactions you process, and how you handle cardholder data. Get this wrong and you’ll either overpay for compliance you don’t need—or underprepare for what’s coming.

Merchant vs Service Provider Classification

Merchants take card payments directly from customers for what they sell. Your fintech app charging subscriptions? That’s merchant territory. You’ll need to secure your payment setup and work with acquiring banks for a Merchant Identification Number (MID).

Service providers handle cardholder data for other businesses. Payment processors, gateways, and fraud tools—if you make transactions happen for someone else, you’re a service provider. Even if you don’t directly touch the data but can influence its security, you still qualify.

Here’s the twist: you might be both if you process your own payments and handle transactions for others.

Transaction Volume and Breach History Criteria

Your 12-month transaction count decides your compliance level.

For merchants:

- Level 1: 6M+ transactions or any breach history

- Level 2: 1–6M

- Level 3: 20,000–1M e-commerce transactions

- Level 4: Under 20,000 e-commerce or under 1M total

For service providers:

- Level 1: 300,000+ transactions or prior breach

- Level 2: Under 300,000

Been breached? You’re automatically bumped higher. The industry doesn’t forget.

Defining Your Cardholder Data Environment (CDE)

Your Cardholder Data Environment (CDE) includes every system, person, and process that touches cardholder data or sensitive authentication info. Assume everything is in scope until proven otherwise—it saves headaches later.

Your CDE usually includes:

- Servers and compute resources

- Payment terminals

- Databases and storage

- Payment apps and APIs

- Access control systems

Network segmentation isn’t required, but skipping it is costly. Without it, your entire network falls under PCI scope—slow, expensive, and overkill. Smart segmentation isolates what matters and reduces compliance effort.

Map every data flow. Track where cardholder data enters, moves, and leaves your environment. This isn’t just paperwork—it’s the foundation of efficient, cost-effective PCI compliance. Do it right now, and future audits and security checks become far simpler.

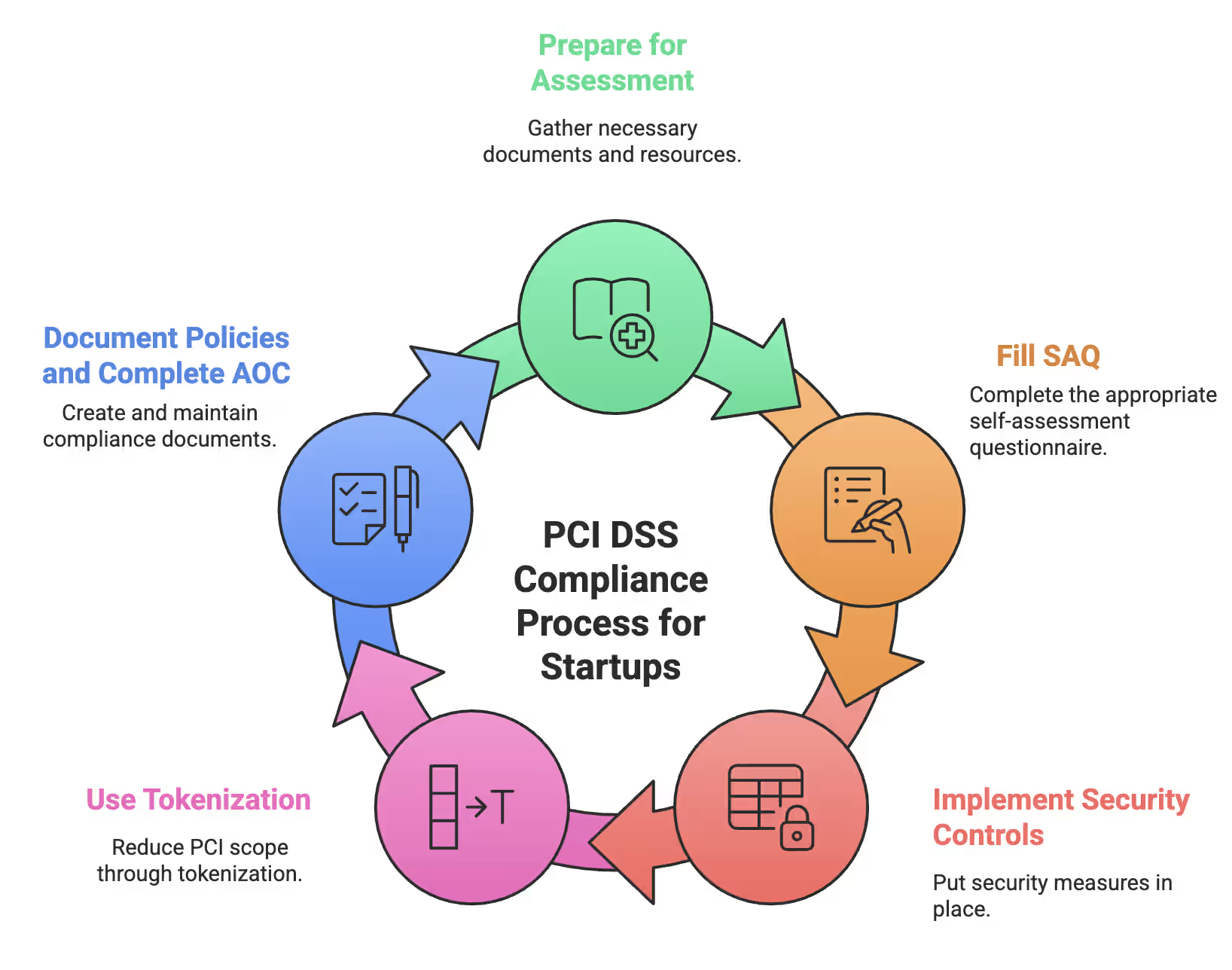

Step-by-Step PCI DSS Compliance Process for Startups

PCI DSS compliance isn’t something you scramble for at the last minute. It’s a structured process that demands planning, documentation, and continuous oversight. For fintech startups, getting this wrong means delays, rework, and potential audit failure.

These are the steps to get your startup PCI DSS compliant:

- Preparing for PCI DSS Assessment

- Filling the Right Self-Assessment Questionnaire (SAQ)

- Implementing Security Controls

- Using Tokenization and Reducing PCI Scope

- Documenting Policies and Completing Attestation of Compliance (AOC)

Let’s get into each of these:

1. Preparing for PCI DSS Assessment

PCI DSS compliance isn’t something you scramble for at the last minute. Early preparation means documenting what matters before auditors ask for it:

- Configuration exports and system screenshots

- Procedural documentation and runbooks

- System logs and proof of ongoing control effectiveness

Run internal checks using SANS PCI checklists to surface gaps early. Bring in Qualified Security Assessors (QSAs) early to align expectations and avoid surprises.

2. Filling the Right Self-Assessment Questionnaire (SAQ)

Most early-stage fintechs complete an SAQ instead of a full audit. Your setup determines the type:

- SAQ A: E-commerce merchants fully outsourcing processing (22 requirements) — payment page is entirely hosted by the processor (e.g., Stripe Checkout redirect, PayPal hosted buttons)

- SAQ A-EP: E-commerce merchants with website-hosted payment pages (~139 requirements) — if your application serves any JavaScript on the same page as a payment iframe, you likely need A-EP, not A. This is where most SaaS fintechs actually land.

- SAQ D: Environments directly handling card data (300+ requirements) — you store, process, or transmit cardholder data directly

Cross 6 million annual transactions and you’ll graduate to a full Report on Compliance (ROC). Expect stricter verification, deeper evidence reviews, and more back-and-forth with QSAs.

3. Implementing Security Controls (Firewalls, Access, and Encryption)

PCI DSS requires strong technical foundations. Core controls include:

- Encryption for data in transit and at rest

- Least-privilege access and periodic access reviews

- Mandatory multi-factor authentication

- Quarterly Approved Scanning Vendor (ASV) scans + internal vulnerability testing

- Active patching and OWASP Top Ten alignment

These controls demonstrate your environment is secured, monitored, and resilient to common attack vectors.

4. Using Tokenization and Reducing PCI Scope

Tokenization removes real card data from your systems, which directly reduces PCI scope by:

- Replacing card data with non-sensitive tokens

- Limiting where card data can exist or move

- Shifting risk to payment or tokenization providers

The result is fewer systems in scope, faster audits, and lower long-term compliance effort.

5. Documenting Policies and Completing Attestation of Compliance (AOC)

PCI DSS also demands formal documentation and executive ownership, supported by policies covering:

- Access control and identity management

- Encryption and key handling

- Logging, monitoring, and incident response

- Secure development and vendor oversight

The Attestation of Compliance is signed by leadership and valid for 12 months. Submitting it signals operational maturity and builds trust with banks and partners.

How Long Does PCI DSS Compliance Take?

Timeline depends on your SAQ type and current security posture:

- SAQ A (4–8 weeks): Document your payment flow, verify full outsourcing, implement the 22 required controls, complete the questionnaire, and submit your Attestation of Compliance.

- SAQ A-EP (8–16 weeks): Additional web application security requirements — script inventory, vulnerability scanning of payment-adjacent pages, and stricter change management — add significant effort beyond SAQ A.

- SAQ D / ROC (6–12 months): Full-scope assessments require gap analysis, remediation across 300+ requirements, penetration testing, and coordination with a Qualified Security Assessor.

Startups with clean cloud-native architectures and tokenized payment flows move faster. Legacy infrastructure, shared environments, or unclear data flows extend the timeline. Either way, start the scoping exercise early — most delays come from discovering systems you didn't know were in scope.

PCI DSS Automation: Simplifying FinTech Compliance

Manual PCI DSS compliance is a time sink. Endless screenshots, spreadsheets, and chasing people for evidence—it drains your team when you should be building product. This is where PCI compliance automation comes in, transforming tedious tasks into seamless workflows.

Automated PCI Compliance and Evidence Collection

PCI DSS automation flips the entire model. Organizations adopting automated compliance workflows have cut evidence-collection hours by up to 80% without replacing their existing GRC tools. How?

- Evidence gets collected, formatted, and uploaded automatically

- Full-population testing replaces risky sample checks

- Tasks flow into Slack/Jira with owners and deadlines

The real win isn’t fancy tooling—it’s systems that generate their own evidence. Add tests, logs, and checks directly into your engineering workflows, and every deployment becomes an audit-ready artifact. As one expert puts it: “For an audit, you just grab the latest run—that’s your evidence.” Clean. Simple. Repeatable.

Real-Time Monitoring and Alerting Capabilities

Continuous monitoring is where automation really earns its keep. Continuous Controls Monitoring (CCM) watches your environment round the clock, catching vulnerabilities, misconfigurations, and unauthorized changes instantly. Automated log monitoring adds another layer—analyzing events across your stack to flag anomalies before attackers can move.

PCI DSS even encourages this. Requirement 10.6 explicitly allows automated log harvesting and alerting. With real-time alerts, compliance violations don’t simmer quietly—they surface instantly.

No more audit-week panic. No more retroactive fixes.

Just a smooth, always-on compliance engine that scales with your fintech.

Benefits of PCI DSS Automation for FinTech Payment Companies

Automation isn’t a luxury anymore—it’s the edge that lets fast-moving fintechs grow without drowning in compliance tasks. While others lose weeks to manual evidence collection, automated teams stay focused on product, customers, and security.

Reducing Manual Compliance Work and Errors

All those screenshots, spreadsheets, and reminder pings? Gone. Automation cuts human effort by up to 80%, enables full-population testing, and automates dozens of PCI controls without scaling headcount. Your security team stops doing admin work and starts doing real security—minus the human errors that derail audits.

Continuous Monitoring and Real-Time Alerts

Security isn’t a quarterly event. Automation gives you 24/7 visibility: instant alerts, File Integrity Monitoring across critical systems, and Continuous Controls Monitoring that tracks drift the moment it happens. You’re not guessing anymore—you know when something breaks.

Faster Audits and Reporting

Audit season becomes painless. Evidence is collected automatically, reports generate themselves, and dashboards show your compliance status in real time. What once took months now takes weeks, with cleaner documentation and fewer surprises.

Enhanced Payment Data Security

Automation doesn’t just save time—it hardens your entire environment. It also strengthens fintech data security, ensuring sensitive cardholder information is protected at every stage. You get early detection of vulnerabilities, continuous enforcement of access and encryption controls, and stronger protection across your CDE.

Your competitors react slowly. You move instantly.

Choosing the Right PCI Compliance Tool for Your Startup

Picking the right PCI compliance tool is a high-stakes decision. Get it wrong and you’re stuck with painful audits, endless manual work, and fines that can hit $100,000 per month. Get it right and PCI becomes a smooth, automated background process while your team stays focused on building product—not chasing screenshots.

Key Features of a PCI Compliance Tool

A solid PCI compliance tool should lift the operational burden from day one and keep your payment environment secure without constant hand-holding. Here’s what that looks like:

- Automated evidence collection so 80% of the manual grunt work disappears.

- Real-time monitoring that flags issues the moment they happen.

- Pre-mapped PCI DSS 4.0 controls so you’re not decoding requirements alone.

- Integrated vulnerability management to surface what actually matters.

- Strong access control + encryption to lock down every place cardholder data lives.

Get these five right, and PCI compliance stops being chaos—and starts becoming predictable.

Comparing Tools: Secureframe, Scrut Automation, and Hyperproof

Not every PCI platform solves the same problem. Some excel at ease of use, others at deep technical checks, and some are built for long-term scalability. Here’s the breakdown—clear, honest, and focused on what actually matters for fintech teams:

Secureframe

Secureframe is built for startups that want PCI compliance without complexity slowing them down.

- Extremely intuitive UI with one of the fastest onboarding flows

- 4.8/5 usability rating from teams that don’t want a steep learning curve

- Strong integrations with AWS, GCP, HRIS tools, and ticketing systems

- Best for founders who want compliance automation that “just works” without heavy configuration

Scrut Automation

Scrut is the most PCI-centric platform, engineered specifically around PCI DSS 4.0’s technical demands.

- Automated checks for open ports, MFA, TLS settings, network segmentation, and config drift

- Real-time monitoring across cloud, endpoints, and access policies

- Access to in-house compliance experts who guide you through PCI audits

- Best for fintechs with complex infrastructure or frequent audits

Hyperproof

Hyperproof stands out for teams planning to scale across multiple certifications.

- 4.9/5 support rating and personalized onboarding help

- Handles PCI, SOC 2, ISO 27001, HIPAA, and more—from one dashboard

- Strong issue-tracking, workflows, and risk management baked in

- Best for growing teams that want one system for all future frameworks

Go with the tool that matches your growth curve—not just the one with the flashiest features.

PCI DSS v4.0: What Changed for Fintechs

PCI DSS v4.0 introduced requirements that hit web-first fintechs especially hard. Three to watch:

Requirement 6.4.3: Script Inventory and Integrity

Every script loading on your payment pages must be inventoried, justified, and integrity-checked. For fintechs using modern JavaScript frameworks with dozens of dependencies, this means implementing Subresource Integrity (SRI) hashes and Content Security Policy (CSP) headers — or explaining why each third-party script belongs.

Requirement 8.3.6: Stronger Password Requirements

Minimum password length increased from 7 to 12 characters. If your application or internal systems still enforce the old minimum, update authentication policies before your next assessment.

Requirement 11.6.1: Change Detection for Payment Pages

You must detect unauthorized modifications to HTTP headers and payment page content. Automated change-detection mechanisms — File Integrity Monitoring (FIM) or tamper-detection scripts — are now mandatory, not optional.

These requirements are enforceable now, not future-dated. If your last assessment was under v3.2.1, expect your QSA to flag these during your next cycle.

Overcoming Common PCI DSS Challenges in FinTech

Automation helps—but fintech comes with challenges that don’t vanish just because you bought a shiny tool.

Avoiding False Positives in Automated Scans

Vulnerability scanners love crying wolf. Your team chases “critical issues” that aren’t real—while actual threats slip by. Routine scans aren’t foolproof. In 2023, over 63% of fintech breaches still involved stolen card data. False positives drain time. Real threats sneak past.

How to fix it:

- Tune scanners to your real environment

- Use proof-based scanning with 99.98% accuracy

- Update scan configs as your infrastructure evolves

Balancing Innovation Speed with Payment Security

Developers push code fast. Compliance wants guardrails. Both are right—but both can clash. And with small businesses folding within six months of a cyberattack, speed can’t come at the cost of security.

How to balance both:

- Build security into dev workflows from day one

- Use DevSecOps to catch issues early

- Segregate environments to limit blast radius

- Use tokenization to shrink PCI scope

Ensuring Secure FinTech Infrastructure Across Teams

Security isn’t just an engineering problem—it’s an everyone problem. One careless click can undo even the strongest tech stack.

Your action plan:

- Run regular penetration tests

- Centralize logs across your payment environment

- Review access controls quarterly

- Create incident response playbooks for cardholder data

- Train teams regularly

Security isn’t a destination. It’s a habit.

Conclusion: Strengthening Payment Security for Startups

PCI DSS compliance isn’t your enemy—it’s your competitive edge. For startups, it might feel overwhelming: determine if you’re a merchant, service provider, or both, map transaction volumes, define your cardholder data environment, document everything, and implement proper security controls.

The difference between winners and casualties? Treat compliance as infrastructure, not overhead. Automation changes the game: real-time monitoring and automated workflows free teams to focus on building products, not chasing audits. Choosing the right tool can make PCI DSS compliance more manageable, whether you prioritize usability, deeper technical checks, or multi-framework support—pick what fits your startup’s needs.

Challenges like false positives, balancing speed with security, or team misalignment are solvable. Configure scanners properly, integrate security into development workflows, and train your team consistently.

PCI DSS is more than a checkbox—it’s trust. Companies that embed it early move faster, win bigger deals, and scale securely. In a landscape of rising customer expectations and regulatory scrutiny, startups that build clean, secure, and smart from day one gain a lasting advantage.

Take control of compliance, reduce risk, and build trust with UprootSecurity—where GRC turns policies and processes into real breach prevention.

→ Book a demo today